China’s State Council Approves 24 New Cross-Border E-Commerce Zones

On December 24, the Chinese State Council released the Announcement of the State Taxation Administration [2019] No. 36 approving the establishment of 24 pilot cross-border e-commerce zones. The document announces the 24 cities, and states that the details of how this will be established and operate will be worked out by the provincial governments.

According to the approval document, the new pilot zones should replicate and promote successful practices adopted by the existing three batches of e-commerce zones and introduce exemptions on value-added tax and consumption tax for retail and exported goods.

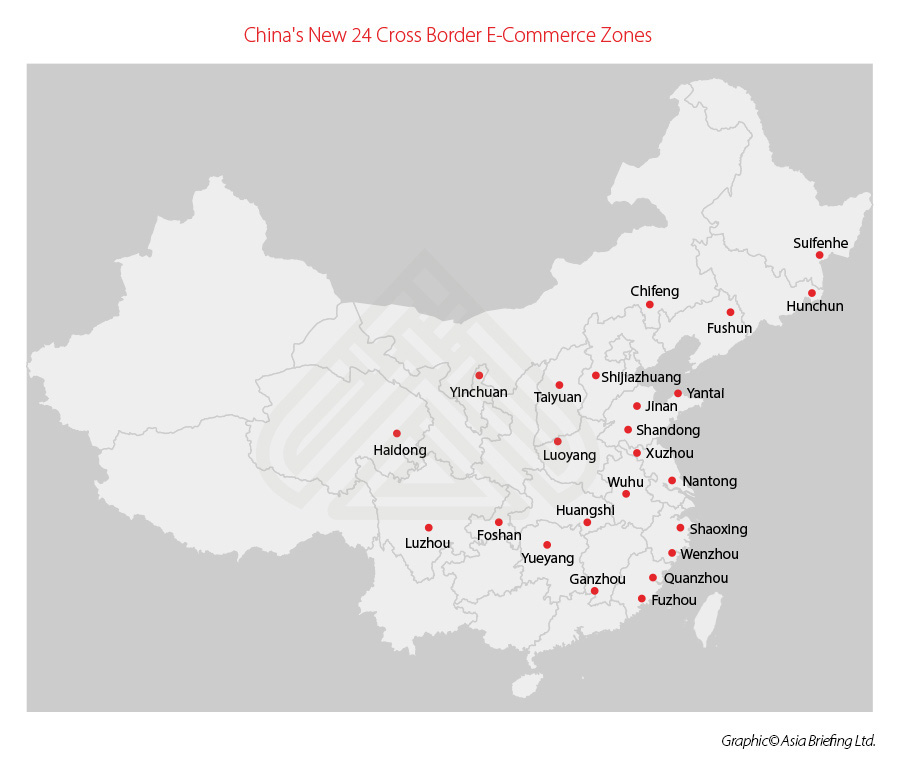

The 24 cities are – Shijiazhuang, Taiyuan, Chifeng, Fushun, Hunchun, Suifenhe, Xuzhou, Nantong, Wenzhou, Shaoxing, Wuhu, Fuzhou, Quanzhou, Ganzhou, Jinan, Yantai, Luoyang, Huangshi, Yueyang, Shantong, Foshan, Luzhou, Haidong, and Yinchuan.

The document is a preliminary announcement and a broad-strokes plan for how these trial zones will be constructed and replicated across the country, with guidance for each provincial government to follow when implementing its own specific measures. More details are expected to follow.

The document itself only alludes to trial related policies on “value-added tax and consumption tax exemption for cross-border e-commerce retail exports, promoting industrial transformation, upgrading and actively carry out exploration and innovation, brand building, and promoting international trade liberalization and convenience.”

However, in October 2019, the State Taxation Administration passed a new corporate tax policy for enterprises within these pilot zones, starting from January 1, 2020. This will likely apply to the 24 cities mentioned above.

According to the document:

- Cross-border e-commerce enterprises subject to tax assessment and collection within the comprehensive pilot zone shall accurately calculate their total revenues, on which corporate income tax will be levied upon assessment at the taxable income rate. The taxable income tax rate shall be four percent.

- Where a cross-border e-commerce enterprise subject to the levy upon assessment of income tax in a comprehensive pilot zone meets the conditions for preferential policies for small low-profit enterprises, it may enjoy the preferential income tax policies for small low-profit enterprises;

- If the income obtained by it is tax-free income specified in Article 26 of the Corporate Income Tax Law of the People’s Republic of China, it may enjoy the preferential policies for tax-free income.

Based on the 35 pilot cross-border e-commerce zones that have previously been established, it is likely that these cross-border zones will adopt similar regulations, including allowing companies to enjoy benefits, such as tax rebates, government support to set up e-commerce platforms, and international logistic services.

China Briefing is written and produced by Dezan Shira & Associates. The practice assists foreign investors into China and has done since 1992 through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Dongguan, Zhongshan, Shenzhen, and Hong Kong. Please contact the firm for assistance in China at china@dezshira.com.

We also maintain offices assisting foreign investors in Vietnam, Indonesia, Singapore, The Philippines, Malaysia, and Thailand in addition to our practices in India and Russia and our trade research facilities along the Belt & Road Initiative.

- Previous Article China Cuts Import Tariffs on Select Goods in 2020, Rates Lower than MFN

- Next Article Corporate Sustainability in China – New Issue of China Briefing Magazine