China’s COVID-19 Recovery: What Lies Ahead for Foreign Investors

Op/Ed by Chris Devonshire-Ellis

While the attention of the COVID-19 pandemic moves away from China, businesses are slowly getting back to normal in the country. That means relief not just for foreign investors based in the country but also for overseas sourcing and manufacturers around the world who are reliant on Chinese supplies.

But how reliable will the return to normality in China be? How long will it last? What are the options?

We deal with these issues in the below sections.

COVID-19: A return to normality

Unlike many commentators on the COVID-19 issue, our firm has several hundred employees and 12 offices in mainland China, plus another in Hong Kong. We also have offices and staff in India, Vietnam, Singapore, Indonesia, Thailand, and Philippines. We have several thousand clients in all regions across China as well as Southeast Asia, and a subscriber base for our Asian-focused websites, such as this, running to 250,000. We are in touch with this pool of on-the-ground resources on a daily basis – meaning we pretty much know what we’re talking about.

There is also precedence. We operated as a business throughout the SARS epidemic in 2003, in addition to the H5N1 outbreak. SARS, while not on the scale of COVID-19, also affected businesses in China – quarantines, towns and villages in lockdown, and factories cutting back production.

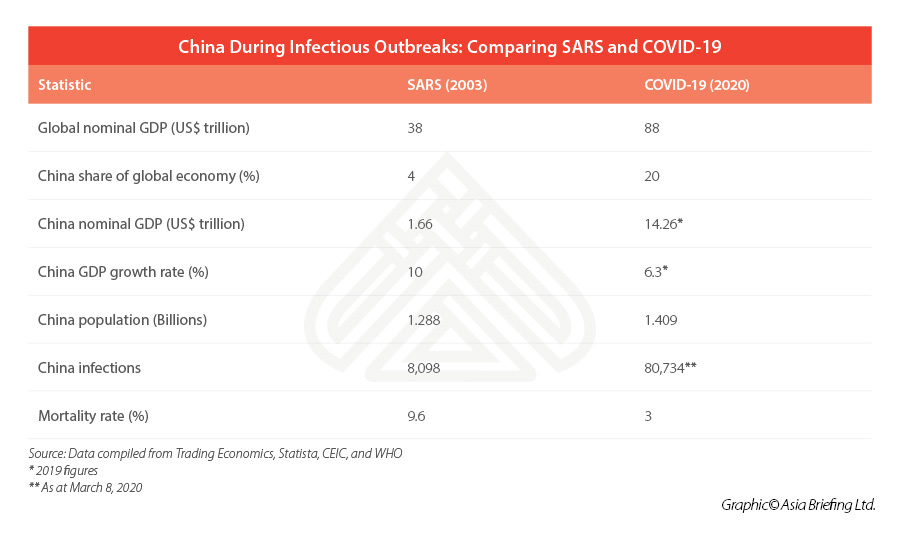

However, China has changed since then as seen in the following table.

What these figures tell us is that the Chinese economy, and its share of total global trade, has quintupled since 2003 and another 120 million people have been added to the population. That’s roughly equivalent to adding another Mexico (129 million), Japan (126 million), or Philippines (109 million) in population over the past 17 years – with most of that attributable in China to an aging population. China’s GDP growth rate has naturally slowed since the 10 percent days of the early to mid-2000’s, while the more infectious nature of COVID-19 over SARS can be seen – it is 10 times more infectious, while the mortality rate is over three times lower.

But what does this tell us?

In essence, China’s share of the global economy has risen and so has the global economy itself – although China’s growth is four times faster than the global average. But still, of the US$50 trillion the global economy grew in that period, China was responsible for just US$12 trillion of that figure. A huge share, but not enough to fully impact the global supply chain as deeply as many believe. And factory complaints aside – have any readers actually noticed anything missing or unobtainable these past few days and weeks? It hasn’t happened – apart from a handful of very silly, front page making disputes about stockpiling toilet rolls.

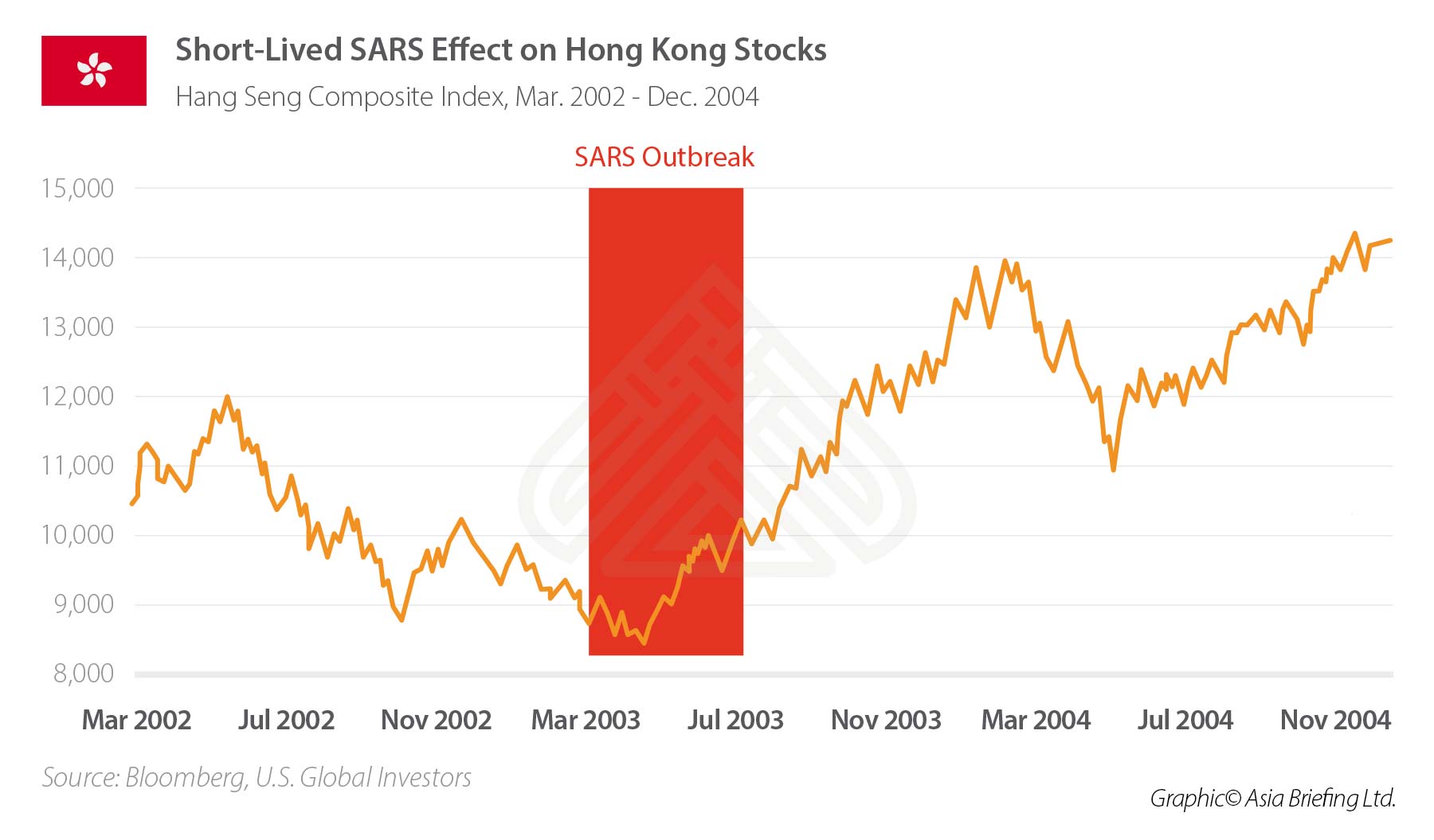

But what happened after SARS? Which after all was, at the time just as scary, impacted China manufacturing and had a far higher fatality rate. This is the performance of Hong Kong’s Hang Seng Index at that time (see below graph).

The rebound from July 2003 has proven both rapid and sustainable – it has never returned to the lows of 2003 and is currently trading at 26,126. Why is this relevant? Because the Hang Seng Index is made up of mainly Chinese A, H, and Red Chips stocks representing the largest Chinese companies, including mainland Chinese banks, telecommunications, energy, construction, IT, engineering, shipbuilding, and retail companies in the country. It is a bellwether of how mainland Chinese businesses are performing. Since March 3 – within the past week – it has risen nearly 100 points.

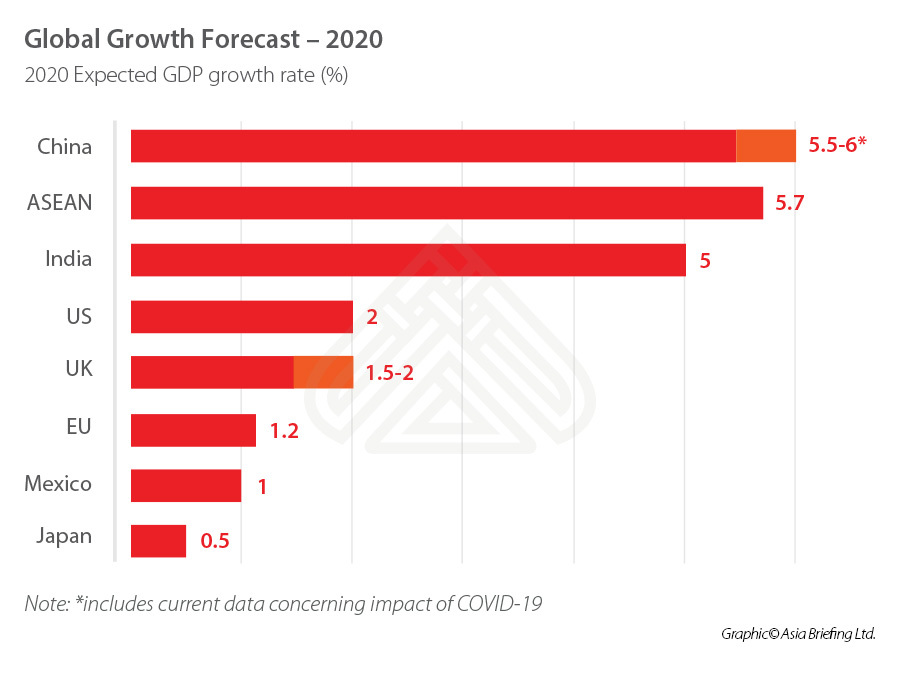

On the ground in China, 90 percent of our staff are back to work in their offices – the remainder are currently overseas due to China travel restrictions or are in China but currently unable to return to work because of internal HR advise in accordance with local official recommendations. COVID-19 has had an impact on our cashflow during January-February this year – 3 percent lower than the same period in 2019. That is not a disaster and will not impact issues such as dividend payments to shareholders and so on. No staff have been laid off, and crucially, and in contrary to what others have said our foreign invested clients have not shown any inclination to leave China. Why? Because despite the COVID-19 issue, China’s 2020 GDP growth is still, even after taking the COVID-19 impact into account, expected to grow by about 5.5 to 6 percent. An overview of differing forecasts from different analysts can be found on CNBC here.

So how does that compare?

The implications are clear. China, along with ASEAN (Southeast Asia) and India, continue to be the global growth hotspots. Now is not a time to be divesting from China operations, and why should you? It still enjoys, despite COVID-19, one of the fastest GDP growth rates in the world – basically triple that of the US and five times faster than Mexico.

Like water for chocolate: The Mexican alternative

In terms of Mexico, we’ve heard of some prospective US law firms approaching American investors in China to decamp there.

We wrote about that in the article China Manufacturing vs. Mexico Manufacturing where we noted Mexican manufacturers are still heavily dependent on Chinese made components, meaning relocating there won’t help a business escape the China dependency. US law firms looking for dead or dying American businesses in China are somewhat predatory in nature and have vested interests in being so. Don’t be fooled.

When comparing Mexico as an alternative market to China, the real comparison is as shown in the table below.

The basic difference between the two markets is that for every 15 middle class Mexicans that can afford to buy a mid-range to luxury product, 550 Chinese people can. This is why it is not a good idea to leave the China market and head to Baja California or any other Mexican manufacturing region as an alternative to China. It just doesn’t make sense. China and Mexico are as different as water and chocolate, to quote Laura Esquivel’s excellent Mexican love story.

There is therefore no need to relocate an existing China production facility to Mexico, or to use a Mexican facility to service a US-based client base. After all, President Trump’s much vaunted US-Canada-Mexico Agreement (USCMA) has not been ratified by any of the parties involved, despite his talking it up as a “great deal”. Meanwhile, Mexico imported US$56 billion worth of products from China last year, second only to Mexican imports from the US. It is important to be on the right side of the equation. Shutting a China factory or dismissing Chinese suppliers when China is Mexico’s second largest source of goods and products just doesn’t make any sense at all, even if the goal is to use a Mexican factory to sell to the US. It still has to source from China to be competitive and sustainable, while US rules of origin laws remain somewhat archaic (1930) and opaque in this arena.

In any event, China and Mexico have a double tax treaty in place, making it a viable option to service the Mexican market from existing China facilities. This document, if applied correctly, can reduce the inherent profits tax on China operations by substituting withholding tax for services rendered by an existing Mexican legal entity. This can reduce China taxes by 10 percent – an attractive proposition – and provide a regular income stream back to the Mexican parent. Contact us for enactment procedures at china@dezshira.com.

What’s next?

COVID-19 is now being contained in China, although worryingly it appears to be spreading in Europe and the US as well as elsewhere. Major events involving global participants may be called off or postponed until 2021. Final calls on that remains to be seen.

However for businesses, and especially those with connections both in and with China, the outbreak should usher in a period of strategic operational reflection and should provide a catalyst for companies working with and in China to enthusiastically adopt the remote working concept, supplemented by the wide range of technology tools already available to increase worker efficiency.

Operating Your China Business During a Crisis and Contagious Disease Outbreaks

Operating Your China Business During a Crisis and Contagious Disease Outbreaks

That means embracing various online technologies – a situation we discussed in some detail in the current issue of China Briefing magazine, which is downloadable here, on a complimentary basis.

The COVID-19 outbreak should, if your business has been negatively affected, provide you with an opportunity to evaluate how you operate and how to get more digitally enabled in your operations. Examining what options are available to you to get the most out of what has already been created and evolve that to maximize effectiveness is the lesson to be learned here.

Meanwhile, the China Manufacturing Purchasing Managers Index (PMI) is another good source of measuring confidence in China’s manufacturing. It runs from 0-100, with a figure below 50, a retraction and above 50, growth. In January this year, it hit middle ground at 50 percent, while last month it shrank to a record low of 35.7 percent – in the given circumstances it is hardly surprising although it usually dips in February anyway due to the Lunar New festivities. March, though, has been different – for most of the month to date, it has been above the 50 percent mark – signaling growth.

The China alternatives in Asia

Nevertheless, we do recognize that for some businesses, the COVID-19 experience coupled with the uncertainty of the US-China trade war may have proven too much, and a new start may be worth exploring. As I pointed out above, it is Asia that is the growth market for products and is still able to provide competitive rates for workers. If you really have reached the end of your China adventures, then there are opportunities. The optimum solution is to combine inexpensive sourcing and manufacturing with the potential for local market development at the same time – sourcing for the US, EU, South American, and African markets while exploiting Asian opportunities too.

ASEAN’s growth rate for this year is expected to be close to 6 percent. India’s at 5 percent. We examined the options available in both, and described market access, legal, and tax positions in the article Fed Up with COVID-19? Here Are the Asian Manufacturing Alternatives, which summarizes the sourcing and production options in India, Indonesia, Philippines, Singapore, Thailand, and Vietnam and contains links to a whopping thirteen complimentary country and investment protocol downloads.

Conclusion

Foreign investors and traders in China have had a tough few weeks, and ought to be able to stand up and be counted for their work in surviving the latest that China has thrown at them. Frankly, this is how emerging markets behave – there are always problems and shortcomings to overcome and sometimes without warning.

So big kudos to all those China expats, and their Chinese staff, and other Chinese workers that have seen the COVID-19 outbreak through. We know how tough that is – well done.

It is always darkest before the dawn, and the start of 2020 has been far from easy. History has shown though that China rebounds fast, and already there are signs that this is occurring.

This recovery, coupled with the still attractive China growth figures, continue to make the country an impressive destination for foreign investment. Now is not the time to pull out and head elsewhere, unless it is part a natural business evolution and expansion. Rather, the COVID-19 outbreak should be a lesson to learn in building in improved efficiencies in your China operations, so it is better prepared, leaner, and more evolved. Closing a China business is a traumatic change; it is far better to adapt what already exists than to terminate. China remains a consumer and growth market to be in. Brighter days are ahead.

Related Reading

About Us

China Briefing is written and produced by Dezan Shira & Associates. The practice assists foreign investors into China and has done since 1992 through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Dongguan, Zhongshan, Shenzhen, and Hong Kong. Please contact the firm for assistance in China at china@dezshira.com.

We also maintain offices assisting foreign investors in Vietnam, Indonesia, Singapore, The Philippines, Malaysia, and Thailand in addition to our practices in India and Russia and our trade research facilities along the Belt & Road Initiative.

- Previous Article COVID-19 in China: Businesses Lose Less, Work Resumes Faster Than Expected

- Next Article Shanghai Moves to Attract Foreign Investment, Open Up China’s Financial Sector